He believes consumption will pick up as several policy moves begin to work together. The Reserve Bank of India has already cut interest rates by 125 basis points and injected liquidity worth around 3% of GDP. While the impact has been slow so far, Sengupta says these steps should start showing up more clearly over the next year.

“We feel pretty good about consumer, especially at the bottom end of the pyramid going into the next year,” he added.

Lower-income households are likely to benefit more. Easier credit, goods and services tax rate cuts, and higher fiscal transfers by state governments — especially around elections — should all help. Together, these could give demand a steady push as FY27 progresses.

Sengupta acknowledged that recent data still looks soft, especially in urban and high-end segments such as housing. But this is because higher-income consumers were already carrying a lot of debt. So, when income tax and interest rate cuts came through earlier, they were mostly used to pay down loans rather than increase spending.

Take housing loans, for instance. Rate cuts often reduced loan tenures instead of monthly EMIs. That meant households focused on cleaning up their balance sheets instead of spending more. Sengupta said this phase is important, because it puts households in a healthier position to borrow and spend later on.

He says early signs of a pickup are already visible. Urban credit growth has started to recover, helped by regulatory easing from the RBI. As households continue to de-leverage over the next six months, this should support a revival in borrowing and spending — especially in the second half of FY27.

Read Here | Goldman Sachs sees strong FMCG recovery, but stays cautious on discretionary demand

On investment, Sengupta does not expect a broad-based private capex revival. Instead, he sees opportunities in specific sectors such as power (both renewable and conventional), electronics, and defence. Public capex growth is likely to slow after heavy front-loading in recent years, but fiscal consolidation may also be less aggressive, reducing the drag on growth.

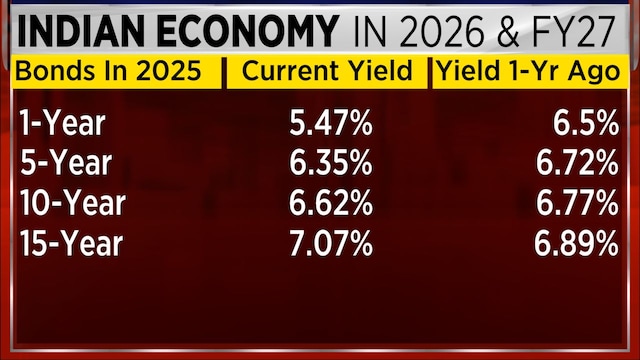

Despite rate cuts, long-term bond yields remain elevated. Sengupta said this is largely due to higher bond supply from state governments and lower demand from insurance and pension funds, which are allocating more money to equities.

He expects the extreme steepness at the long end of the yield curve to ease somewhat over the next year, although large further declines may be limited as the RBI is near the end of its rate-cut cycle.

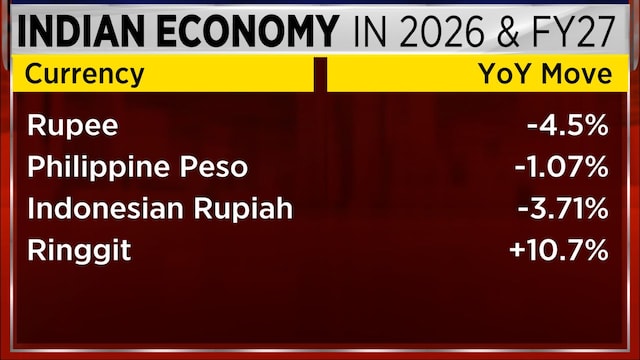

Sengupta said the recent rupee depreciation was a needed adjustment after earlier overvaluation. With valuations now more attractive, he expects capital flows to improve and does not see a third consecutive year of balance-of-payments deficit.

This, along with policy support, should help India grow at late 6% levels in FY27, even if global uncertainties persist.

For full interview, watch accompanying video