Passenger vehicle sales grew to around 45.8 lakh units in 2025, up about 6 percent year-on-year. SUVs continue to expand their lead, crossing 55 percent market share, but sedans show a small rise in market share despite fewer new launches and sustained pressure from the SUV segment.

Of 27 launches in 2025, only one is a sedan, whereas SUVs make up more than half and EVs account for over 40 percent of all new models.

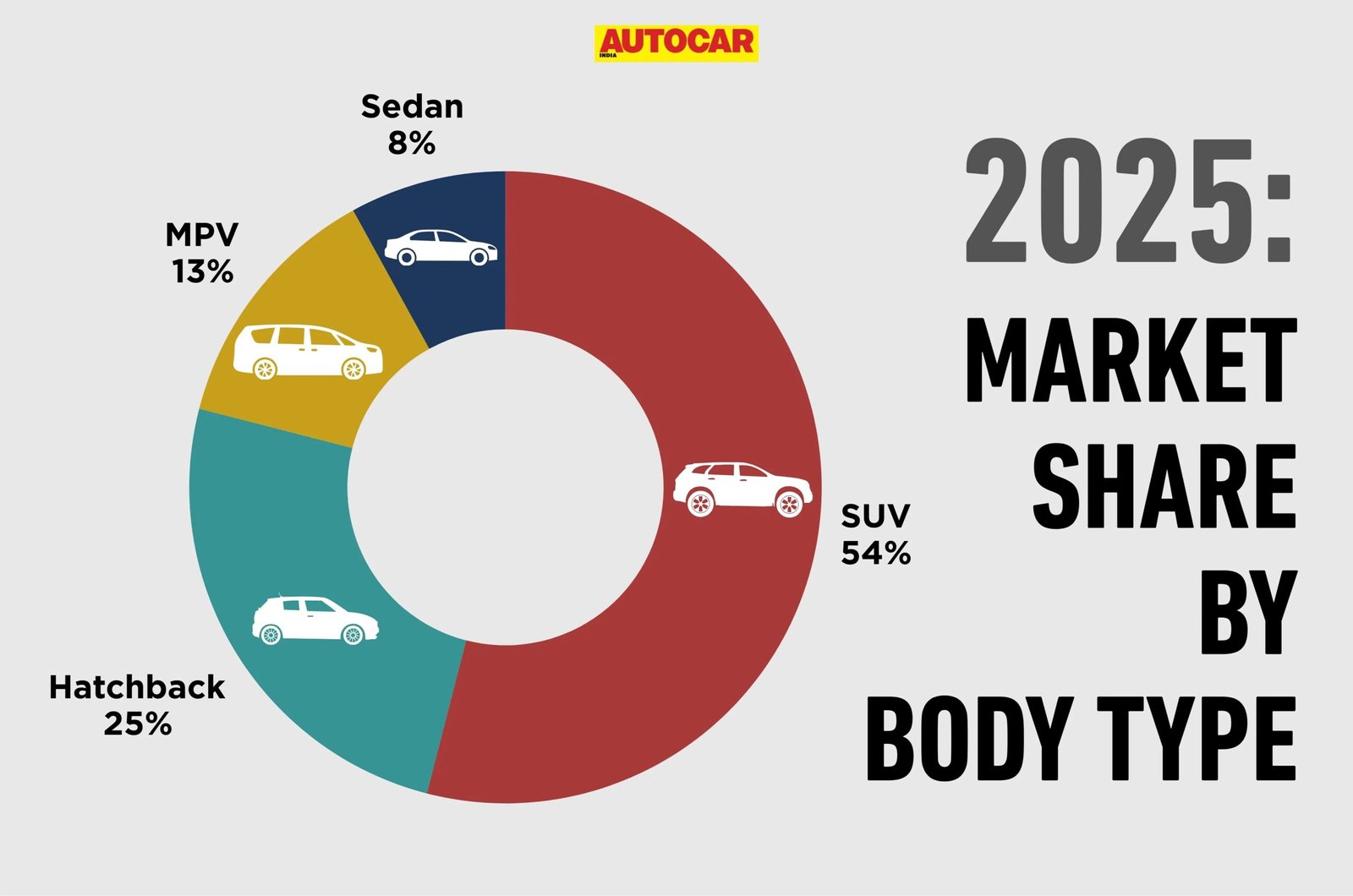

Sedans hold steady despite limited new launches

Compact and midsize models anchor demand; Dzire becomes best-selling car in 2025

Sedan share increased from 8 to 8.6 percent in 2025, supported by steady demand across compact and midsize sedans, including the Maruti Dzire, Hyundai Aura, Tata Tigor, Honda Amaze, Hyundai Verna, Volkswagen Virtus, Skoda Slavia and Honda City.

These models continue to attract buyers who prioritise comfort, space and a traditional three-box layout over ground clearance and stance. Turbo-petrol versions of the Verna and Slavia/Virtus also cater to buyers seeking stronger performance.

The Dzire stood out as India’s best-selling car in 2025, becoming the only sedan since 2020 to top the annual sales charts, highlighting its continued relevance despite the wider shift towards SUVs.

With only one new sedan launching in 2025, the Skoda Octavia RS in limited numbers, existing models were enough to hold sedan share even as SUVs dominated new launches.

SUV growth slows

Smaller year-on-year increase helps other segments hold their ground

SUV share rises from 54 to 55.4 percent, but the pace of growth is slower than in recent years. This suggests that SUV demand, while dominant, may be approaching a plateau, allowing other body styles to maintain share rather than lose ground every year.

SUVs continue to dominate new product activity, with 15 out of 27 new launches this year coming from this segment.

Hatchback sales continue to drop

Compact and sub-compact SUVs leave hatchbacks with limited appeal

Hatchback share falls from 25 to 22.8 percent, extending a multi-year slide as buyers move towards compact SUVs. The segment saw little fresh product activity, with most models carrying over without major updates, barring the Tata Altroz facelift.

Despite the GST cut, entry-level hatchbacks such as the Alto and S-Presso remain price-sensitive, which has limited growth in the segment even as the overall market expanded.